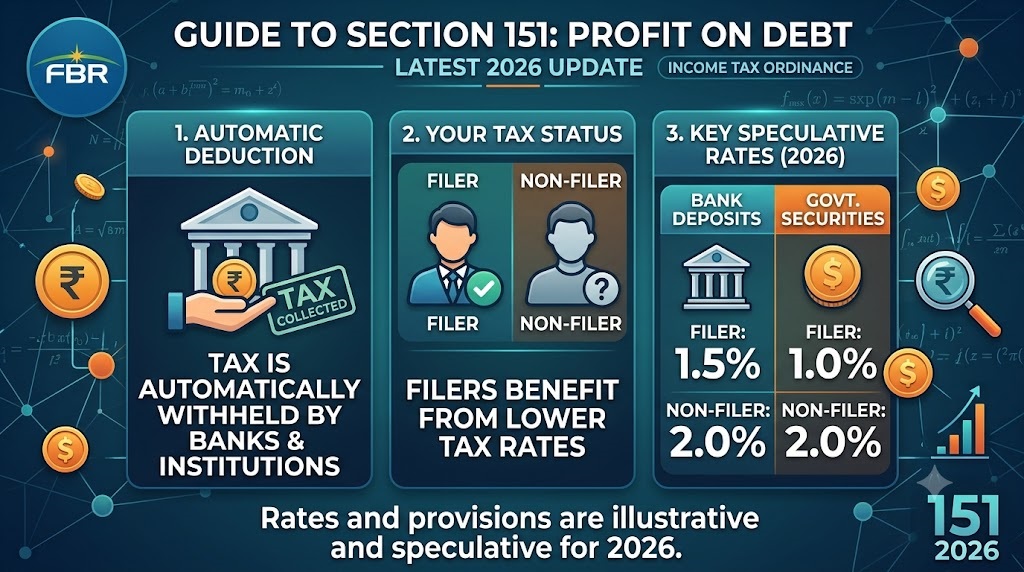

Section 151 of the Income Tax Ordinance deals with tax deducted on profit earned from banks or financial institutions.

Most individuals see this deduction on bank profit or savings accounts but do not fully understand how it works or how it is adjusted in tax returns.

This article explains the mechanism in a simple way so you can correctly manage it in your income tax filing.

What Section 151 Actually Means (Profit on Debt Tax)

Section 151 applies to “profit on debt,” which mainly includes:

- Bank interest on savings accounts

- Profit from fixed deposits (TDRs)

- Return on financial savings instruments

Banks and financial institutions deduct tax before paying you the profit.

This deduction is sent directly to the Federal Board of Revenue (FBR).

In simple terms:

You don’t pay it yourself — it is automatically withheld by the bank.

How Banks Deduct Tax Under Section 151

When you earn interest or profit from a bank, the bank acts as a withholding agent.

The process works like this:

- Bank calculates your profit on savings or investment

- Applies withholding tax rate as per FBR rules

- Deducts tax before crediting your account

- Deposits the deducted amount with FBR

This means your bank statement will always show net profit after tax deduction.

The rate of tax may vary depending on your tax filer or non-filer status.

How to Adjust Section 151 Tax in Your Income Tax Return

This tax is not a final tax in most cases.

If you are a filer, you can adjust it when filing your annual return.

Here’s how it works:

- You declare bank profit in your income tax return

- You also report tax already deducted under Section 151

- FBR gives credit for the deducted tax

- It reduces your total payable tax liability

If you do not declare it, you may lose the adjustment benefit.

Common Mistakes Taxpayers Make

Many people face issues because of simple errors:

- Not declaring bank profit in return

- Ignoring withholding tax already deducted

- Treating it as final tax without checking filer status

- Mismatch between bank certificate and return data

Correct reporting ensures you don’t pay extra tax.

FAQ

1. What is Section 151 of the Income Tax Ordinance?

It is the section that deals with withholding tax on profit earned from banks and financial institutions.

2. Is bank profit taxable in Pakistan?

Yes, bank profit is taxable and tax is usually deducted at source under Section 151.

3. Can I adjust Section 151 tax in my return?

Yes, filers can adjust it in their annual income tax return as tax already paid.

4. Who deducts tax under Section 151?

Banks and financial institutions deduct this tax before crediting profit to your account.

5. What happens if I don’t file a return?

You may not get adjustment benefits and could pay higher effective tax.

This topic is part of a complete guide on Income Tax Return Filing Services